Fascination About Tulsa Ok Bankruptcy Specialist

The Main Principles Of Tulsa Bankruptcy Attorney

Table of ContentsGetting The Bankruptcy Law Firm Tulsa Ok To WorkTulsa Ok Bankruptcy Specialist Fundamentals ExplainedWhat Does Chapter 7 Vs Chapter 13 Bankruptcy Mean?The smart Trick of Chapter 7 - Bankruptcy Basics That Nobody is DiscussingGet This Report on Bankruptcy Lawyer Tulsa

The stats for the various other primary kind, Phase 13, are also worse for pro se filers. Suffice it to claim, talk with a lawyer or 2 near you that's experienced with bankruptcy regulation.Many attorneys additionally provide complimentary examinations or email Q&A s. Take advantage of that. Ask them if bankruptcy is indeed the best option for your circumstance and whether they believe you'll qualify.

Advertisements by Cash. We might be compensated if you click this ad. Ad Since you've chosen bankruptcy is without a doubt the best training course of activity and you hopefully removed it with a lawyer you'll need to start on the documentation. Before you dive right into all the official personal bankruptcy types, you ought to get your very own papers in order.

Some Ideas on Tulsa Bankruptcy Consultation You Need To Know

Later down the line, you'll really require to show that by divulging all type of info regarding your economic events. Right here's a standard list of what you'll require on the road ahead: Determining files like your chauffeur's certificate and Social Safety card Income tax return (approximately the previous 4 years) Evidence of earnings (pay stubs, W-2s, freelance earnings, earnings from assets in addition to any kind of earnings from federal government advantages) Financial institution statements and/or retirement account declarations Evidence of worth of your assets, such as vehicle and property appraisal.

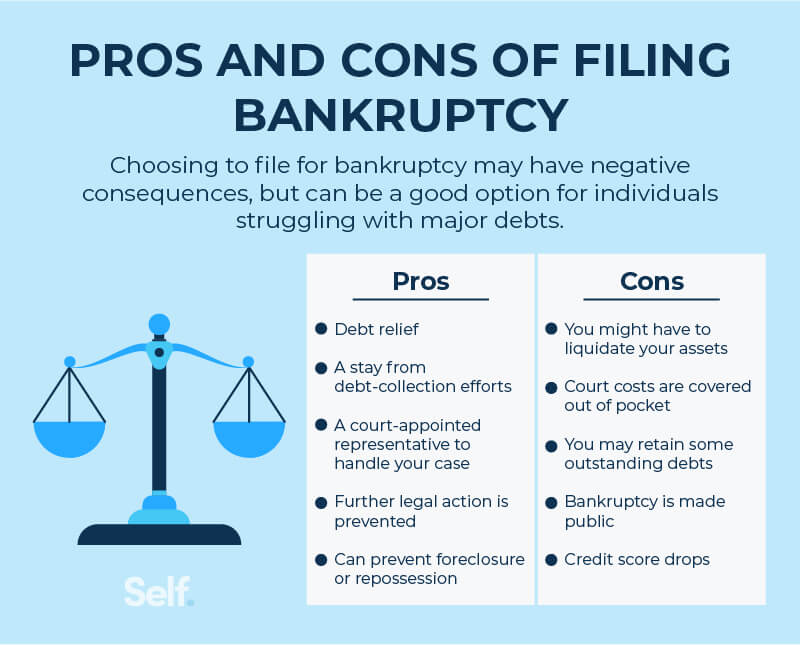

You'll desire to comprehend what kind of debt you're trying to solve.

You'll desire to comprehend what kind of debt you're trying to solve.If your earnings is too expensive, you have an additional choice: Phase 13. This choice takes longer to resolve your debts since it needs a long-lasting settlement plan typically 3 to 5 years prior to a few of your staying debts are cleaned away. The filing procedure is additionally a lot a lot more intricate than Chapter 7.

Some Known Facts About Top Tulsa Bankruptcy Lawyers.

A Chapter 7 bankruptcy stays on your credit score record for 10 years, whereas a Chapter 13 insolvency drops off after 7. Both have long-term influence on your credit history, and any new financial debt you take out will likely include greater rate of interest. Prior to you submit your personal bankruptcy types, you need to initially finish an obligatory training course from a credit scores therapy firm that has been approved by the Division of Justice (with the significant exemption of filers in Alabama or North Carolina).

The program can be finished online, face to face or over the phone. Training courses normally cost in between $15 and $50. You should finish the training course within 180 days of filing for bankruptcy (Tulsa bankruptcy lawyer). Utilize the Division of Justice's site to find a program. If you stay in Alabama or North Carolina, you should choose and complete a course from a listing of separately authorized suppliers in your state.

The smart Trick of Tulsa Bankruptcy Attorney That Nobody is Discussing

Check that you're filing with the right try this out one based on where you live. If your copyright has relocated within 180 days of loading, you must submit in the district where you lived the greater section reference of that 180-day duration.

Typically, your bankruptcy attorney will work with the trustee, but you may require to send out the individual files such as pay stubs, tax obligation returns, and bank account and debt card declarations straight. A typical misconception with personal bankruptcy is that as soon as you file, you can quit paying your financial obligations. While personal bankruptcy can help you wipe out many of your unsafe financial obligations, such as past due medical bills or individual lendings, you'll want to keep paying your month-to-month payments for safe financial obligations if you want to maintain the home.

The Greatest Guide To Chapter 7 Vs Chapter 13 Bankruptcy

If you go to threat of repossession and have actually tired all various other financial-relief alternatives, after that applying for Phase 13 might postpone the foreclosure and help save your home. Inevitably, you will still require the income to continue making future home loan settlements, as well as paying back any type of late settlements over the training course of your payment plan.

If so, you might be called for to give extra info. The audit could delay any kind of financial debt alleviation by a number of weeks. Obviously, if the audit shows up inaccurate info, your situation could be dismissed. All that said, these are relatively uncommon instances. That you made it this far at the same time is a suitable indication a minimum of several of your debts are qualified for discharge.